Sundry Photography/iStock Editorial via Getty Images

Introduction

There’s one group of investors that I tend to “neglect” every now and then, and that’s high-yield-seeking investors. As I’m mainly focused on quality dividend growth, a lot of stocks that I cover don’t yield more than 2-2.5%. In this article, I’m going to present a high-yield stock that’s not just high-yielding, but also capable of growing its business on a long-term basis, buying back shares, and benefiting from the ongoing energy crisis. That company is Valero Energy (NYSE:VLO), one of America’s largest refining companies. The company has a high yield (>3%), a fantastic business model capable of long-term growth, and a huge tailwind from the ongoing energy crisis, which is boosting margins and allowing the company to reduce debt at a pace faster than what anyone could have guessed prior to 2022. In this article, I will guide you through my thoughts and explain why Valero is one of my favorite companies despite my focus on dividend growth over yield.

The title of this article isn’t clickbait, at all. I believe that Valero Energy offers the best of two worlds – high yield and dividend growth. It even comes with a great valuation!

With a market cap of $46.7 billion, San Antonio-based Valero is one of the nation’s largest refinery companies.

Valero Energy

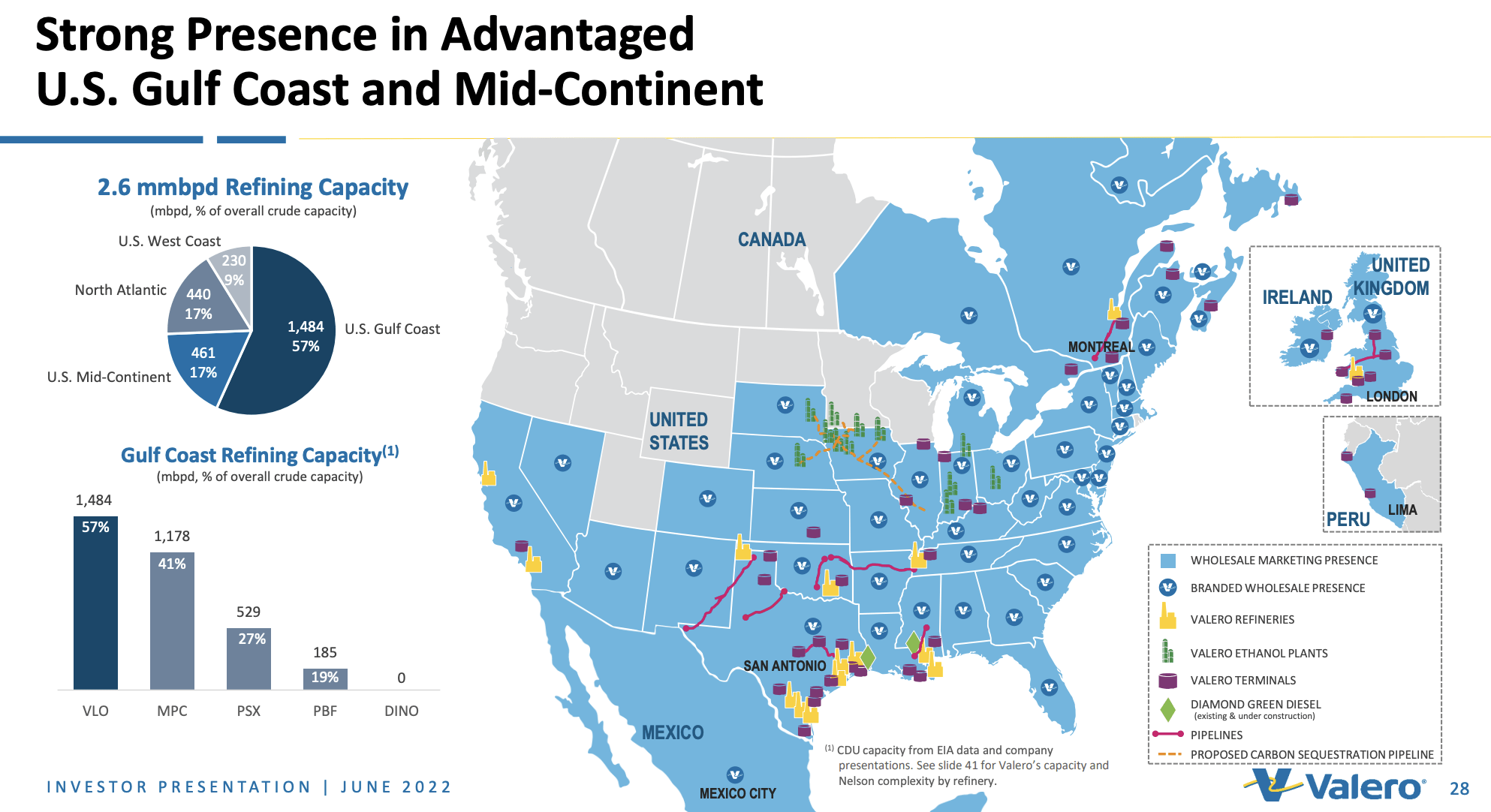

The company has three operating segments, refining, renewable diesel, and ethanol. The ethanol segment dominates the ethanol hub of the world, the US Midwest as the map above shows.

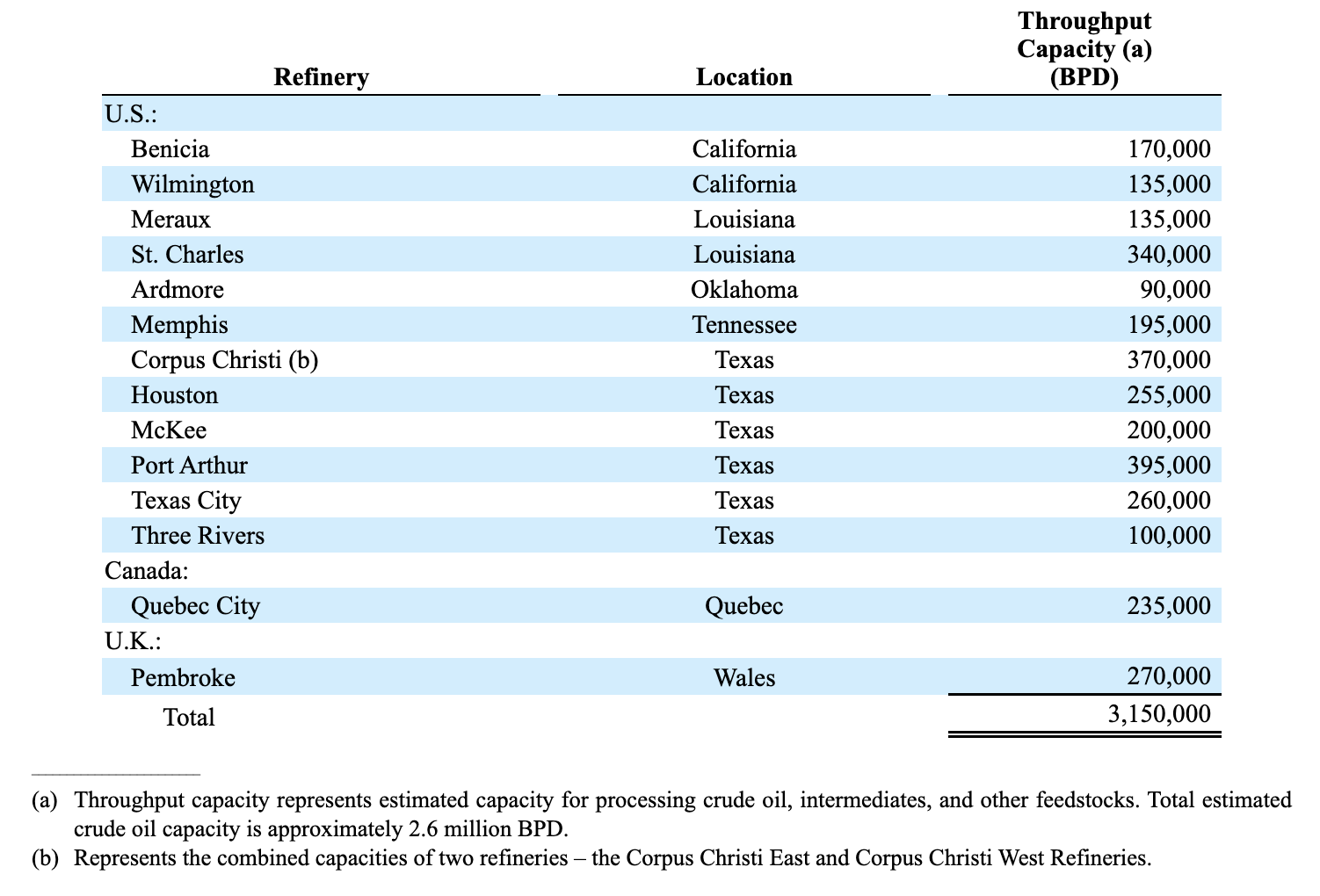

The company has 15 petroleum refineries located in the US, Canada, and the UK with an annual throughput capacity of 3.2 million barrels per day.

Valero Energy

This segment is the company’s bread and butter as it generated 94% of 2021 sales.

In its renewable diesel segment, the company works with its joint venture DGD – Diamond Green Diesel – which has operations in Louisiana. This plant turns “waste” and renewable materials into diesel.

DGD began an expansion of the DGD Plant in 2019 and operations commenced in the fourth quarter of 2021. This expansion increased the DGD Plant’s renewable diesel production capacity by 410 million gallons per year, bringing DGD’s total renewable diesel production capacity to 700 million gallons per year, and provided DGD with the ability to produce 30 million gallons per year of renewable naphtha. Renewable naphtha is used to produce renewable gasoline and renewable plastics.

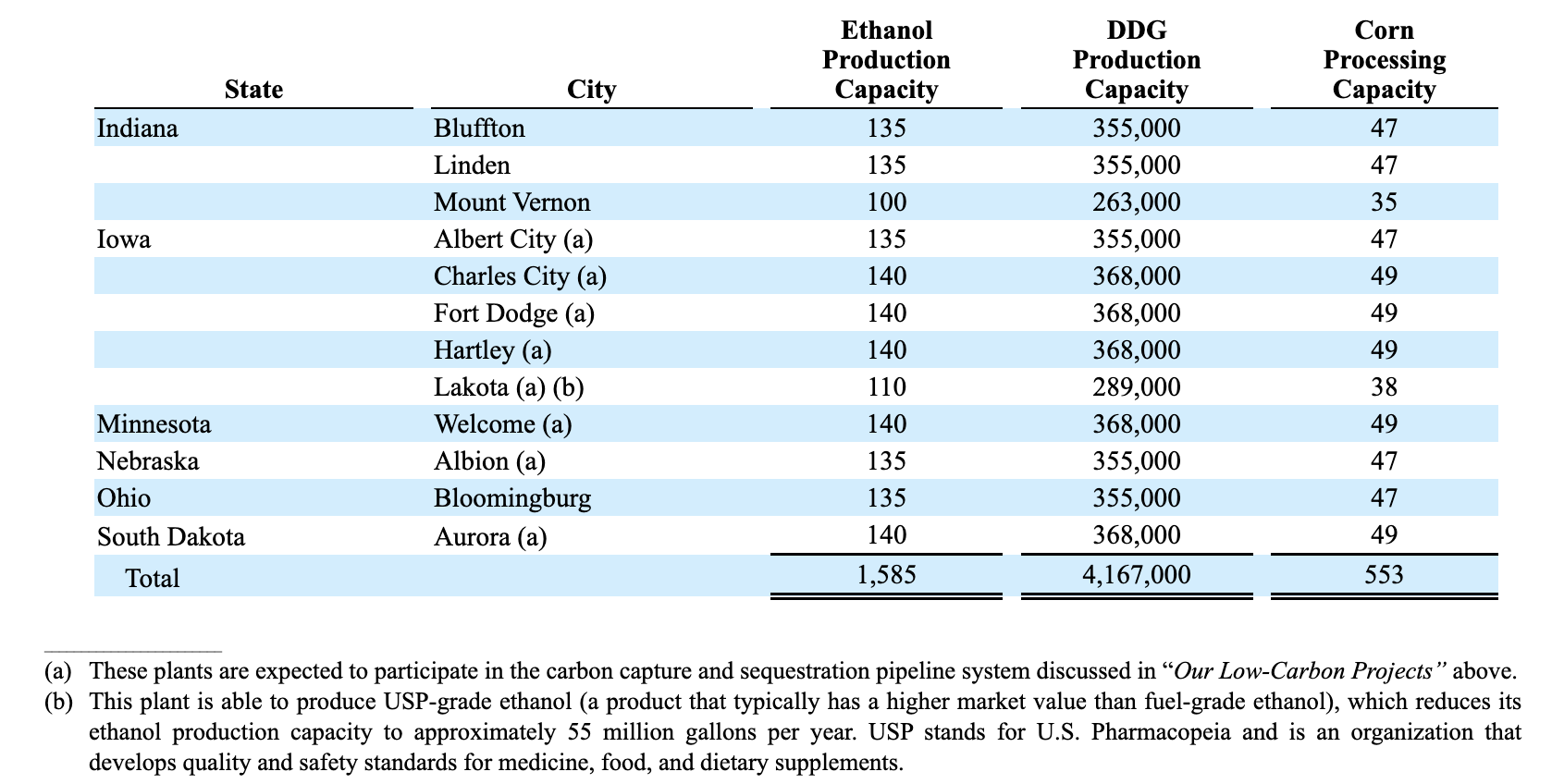

On top of that, Valero is one of America’s top ethanol producers. Like renewable diesel, ethanol is a clean energy source, and the backbone of America’s agriculture industry as a big part of annual corn production is turned into ethanol. Valero has a corn processing capacity of 553 million bushels, which feeds 12 plants in the Midwest producing 1.6 million gallons of ethanol per year and 4.2 million tons of DDGs, which stands for dried distillers grains.

Valero Energy

Sky-High Shareholder Value

Given the size of its refining segment, Valero is driven by two things. First, refined volumes and, second, margins.

If we ignore natural disasters, volume is mainly driven by economic growth. Higher economic growth requires more energy. Margins are driven by a wide range of factors.

In this case, it’s tight supply and the return of demand.

As I wrote last month, the crack spread is at extremely elevated levels.

The so-called 3-2-1 crack spread shows what we can expect in terms of refinery profitability. In this case, 3-2-1- stands for the cost of 3 crude oil future contracts, 2 gasoline futures contracts, and 1 ULSD diesel futures contract. If refined product prices rise faster than the price of oil, refineries make more money when buying a barrel of oil. After all, Valero does not produce oil, it buys feedstock for its operations consisting of “traditional” refining, renewable diesel, and ethanol.

As a benchmark, I’m using CME’s RBOB Gasoline Crack Spread Futures. Although the crack spread is well-below its 2022 highs, the spread remains at elevated levels. The current spread is roughly $10 per barrel above prior cycle highs.

TradingView (ARE Crack Spread Futures)

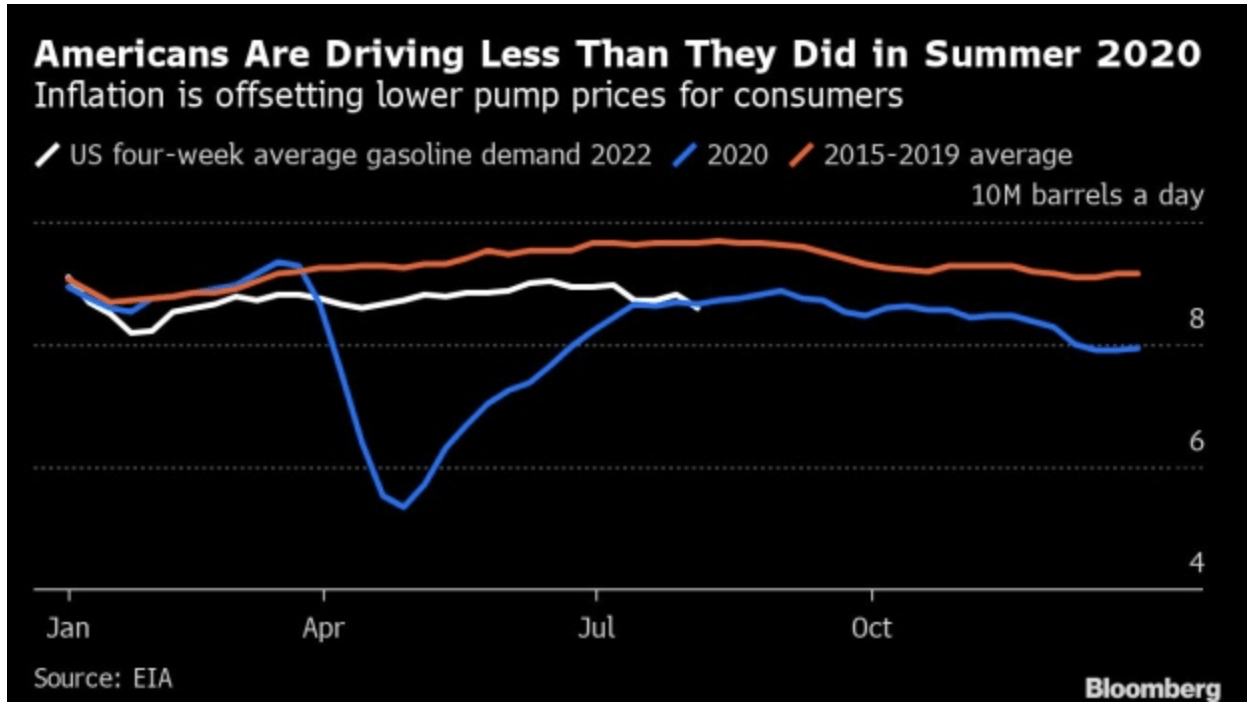

So far, this is leading to gasoline demand weakening as prices were too high for consumers. It also has something to do with general economic weakness, but I will get to that towards the end of this article.

Bloomberg

For now, Valero benefits from a tight industry supply. Not only is worldwide oil supply an issue as I discussed in articles like this one, but the main bottleneck is refinery capacity.

One of the most important drivers of margins in the industry is the fact that we’re still suffering from pandemic-related capacity shutdowns. Back in 2020, major refinery companies around the globe decided to shut down. Maintaining refineries is extremely expensive (VLO wasn’t even able to cover maintenance costs with operating cash flow in 2020), and the outlook was uncertain. Hence, capacity was shut down.

In 2021, global refinery capacity fell by 730 thousand barrels per day. That’s the first decline in 30 years.

In the United States, refining capacity has decreased by about 1.1 million b/d since the start of 2020, contributing 184,000 b/d to the global decline in 2021. Global demand for refined products dropped substantially in 2020 as a result of the COVID-19 pandemic. Less petroleum demand and the associated lower petroleum product prices encouraged refinery closures, reducing global refining capacity, particularly in the United States, Europe, and Japan.

With these numbers in mind, the IEA (don’t confuse this with the American EIA), estimates that *net* refinery capacity is set to expand by 1.0 million barrels per day in 2022 and 1.6 million barrels per day. China and the Middle East are expected to add 4.0 million *gross* barrels per day during this period.

In other words, the difference between net and gross is roughly 1.4 million barrels per day over the next 2 years, which indicates that supply is set to remain tight in western countries.

The only expansion in western countries is in Beaumont, which is owned by Exxon Mobil (XOM).

EIA

As a result of a tight market and (related) high margins, the company easily offsets weakness in demand.

For example, in 2Q22, the company did $51.6 billion in revenue. An increase of 86.2% year-on-year and $10.9 billion higher than expected. Again, $10.9 BILLION higher than expected.

This helped the company to do $11.36 in non-GAAP EPS, which was beaten by $2.16.

In its refining operations, operating income hit $6.2 billion versus $349 million in the second quarter of 2021. Moreover, volumes were strong as Valero produced 3.0 barrels per day, up 127 thousand barrels per day versus 2Q21.

The company achieved a refinery margin of $30.01 per barrel, which is up from $7.95 in the prior-year quarter. Adjusted refinery operating income per barrel (after expenses like depreciation) was $22.71, up from $1.71.

The total utilization rate was 94%, up from 74% in 2Q21.

Moreover, the company confirmed “my” bull case, as it mentioned supply issues facing the industry:

Product supply is constrained as a result of significant refinery capacity rationalization that was triggered by the COVID-19 pandemic, driving the shutdown of marginal refineries and conversion of several refineries to product low-carbon fuels. In addition, the Russia-Ukraine conflict intensified the supply tightness with less Russian products in the global market.

With that said, even if this environment does not last (margins will come down as supply rebounds), we’re in an absolutely fantastic environment for shareholders. Valero’s financials are looking fantastic and allowing the company to reduce debt much faster than previously anticipated.

Below, you’re looking at a number of related financial numbers. The most important two are free cash flow and net debt. Free cash flow is basically operating cash flow minus capital expenditures (CapEx). As we see, the company is maintaining steady CapEx. Roughly 60% of this CapEx is sustaining CapEx to maintain current operations. 40% is growth CapEx. Half of that is CapEx going into renewable projects.

In 2020, the company didn’t even have enough money to sustain its operations. Now, the company is on track to do $9.8 billion in free cash flow. That’s 21% of Valero’s current stock price.

TIKR.com

This much free cash flow won’t last, but my point is that Valero can (and will) use this to reduce debt. This year, the company is set to reduce net debt to $5.1 billion. Since 2020, the company has reduced gross debt by $2.3 billion, including $300 million in June alone. In 2020, it incurred $4.0 billion in incremental debt to sustain operations and its dividend (there was NO dividend cut in 2020).

What this means is that the company is set to end up with a healthier balance sheet than in 2019. This is set to continue, even as free cash flow comes down. By 2024, Valero is not expected to have more than $2.8 billion in debt – or less than 0.4x EBITDA.

Moreover, if the company continues to do more than $4.0 billion in free cash flow in “normal” years, we’re dealing with a free cash flow yield of close to 9%.

This brings us to the question, what about the dividend?

The VLO Dividend

I bought Valero in 2020, which means it’s one of two stocks in my portfolio that has not raised its common quarterly dividend.

Some think that’s a bad thing, I think it makes total sense. After all, the company did not cut its dividend in 2020. If the company had cut, we would require (I assume) high dividend growth just to get back to 2019 levels.

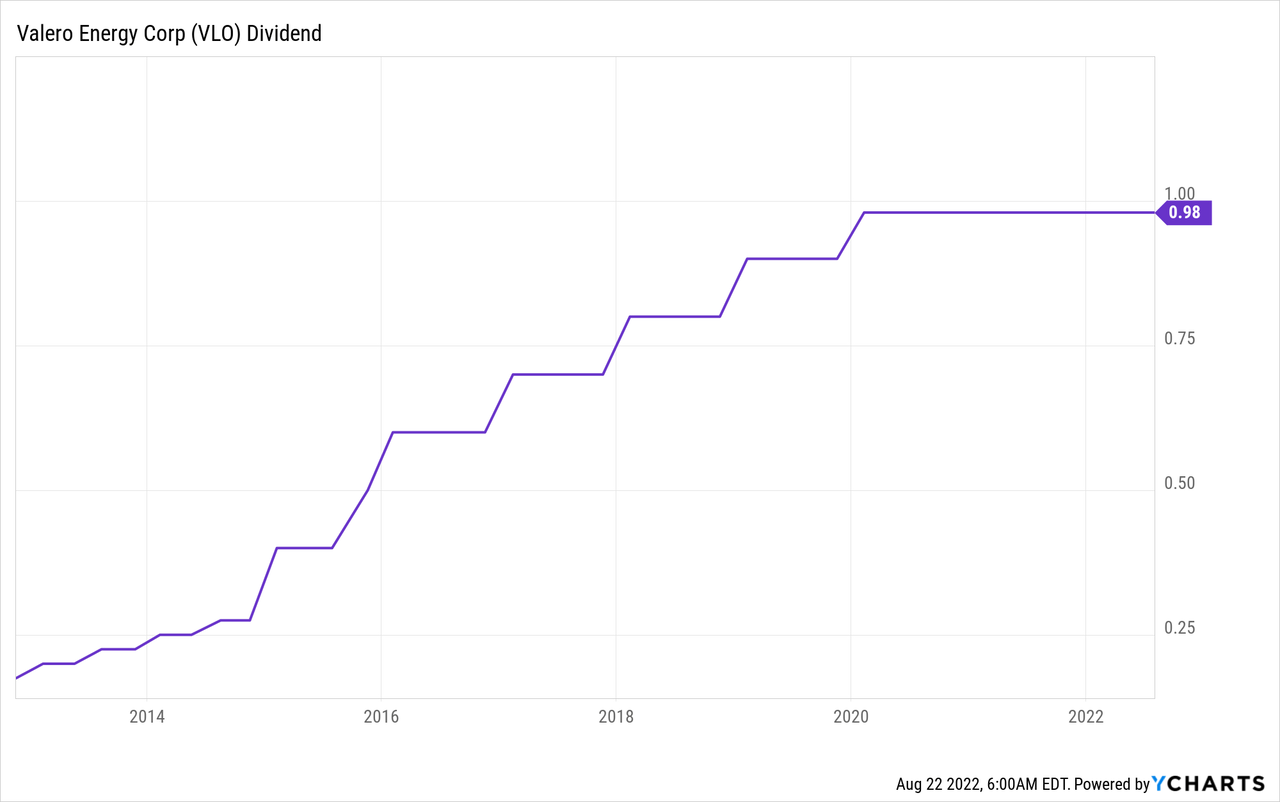

Now, we’re not enjoying dividend hikes, but a high dividend. Even though Valero is up 57% year to date, its dividend yield is 3.3% based on a $0.98 per quarter per share dividend. 3.3% isn’t extremely juicy, but it’s a high yield.

And, even more important, there is so much room to improve the dividend as the free cash flow and debt numbers (that I just showed you) confirm.

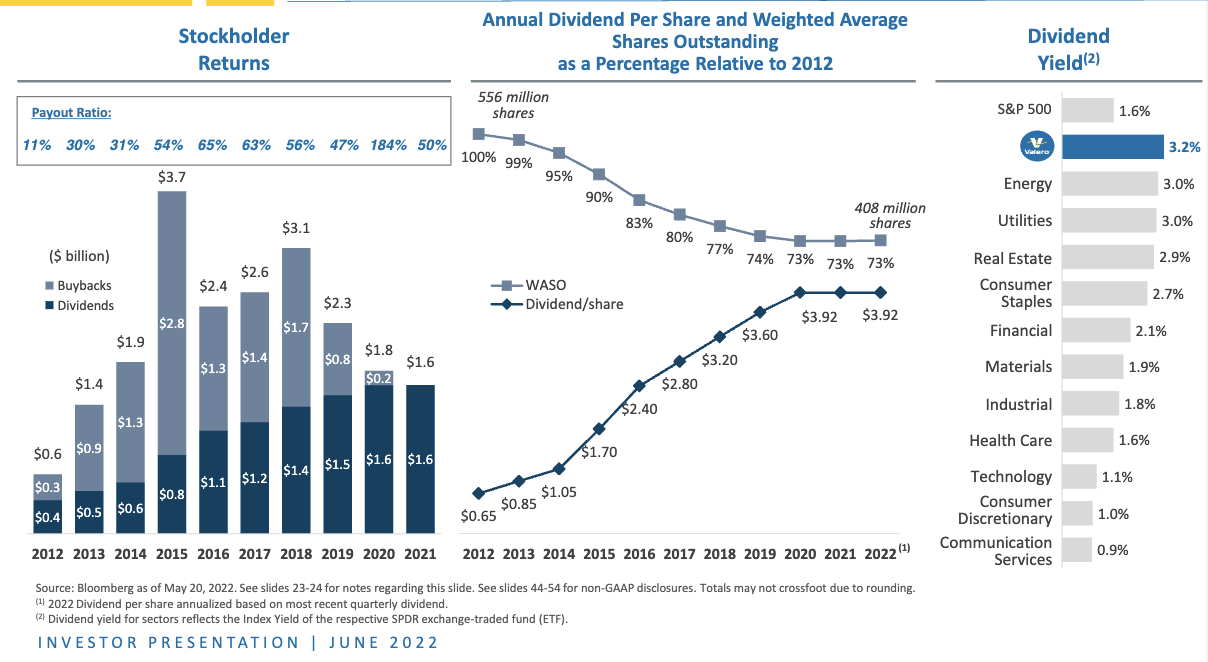

What matters to me is that we’re not buying a company with a high yield but no growth. Valero’s 10-year average dividend growth rate is 24%. That’s absolutely wild and not sustainable. Yet, it shows that Valero is very serious about returning cash. When it has the chance to accelerate distributions, it does exactly that.

The most “recent” dividend hikes are:

January 2020: +8.9% (a month before COVID hit)

January 2019: +12.5%

January 2018: +13.3%

In other words, unless the world is in a deep recession, the company rewards its investors with double-digit dividend hikes. Hiking a 3.3% yield with 10% turns the yield into a 3.6% yield. In other words, “high-yield” very quickly becomes an even higher yield.

Now, the question on everyone’s mind is: when are we going to get a hike? Or buybacks? After all, both forms of distributions have come to a grinding halt when we got bad news from Wuhan two years ago.

In 2Q22, the company returned 42% of adjusted net operating cash through dividends and buybacks. That’s close to the lower range of the 40-50% targeted payout ratio.

This payout ratio was only achieved because buybacks were boosted to $1.7 billion, the first significant buyback since the start of the pandemic.

Bear in mind that buybacks have “always” been a key tool for VLO to distribute cash. Between 2012 and 2020, roughly 27% of total shares were bought back.

Valero Energy

Anyway, to return to the key question – when are dividend hikes coming back? – the answer is vague.

Roger Read, a Wells Fargo analyst, asked the following question:

Okay. And just maybe as one little tweak on that, as you think about dividend versus share repos, does that ultimately change once the balance sheet is back the way you wanted — it’s been a while since you’ve increased the dividend, I guess, is really what I’m getting at. Should we think of that as becoming another way to return cash?

The company answered:

Yes, I mean, you should. That is something we’ll be looking at, as we’ve discussed, our short-term focus is on getting the debt back down. And we will look at that. We met and looked at this before. We’ll be measured in our approach to ensure it’s something that’s sustainable through this cycle, especially given what we experienced coming through COVID, but that is something we’ll be looking at.

In other words, when debt comes down, dividend hikes will return. For now, buybacks will have to do the job. My personal opinion is that we will get a juicy hike in January of 2023. The balance sheet has become sustainable and unless the economy tanks, I don’t see a reason why Valero shouldn’t be able to return to annual January hikes.

Valuation & One Major Headwind

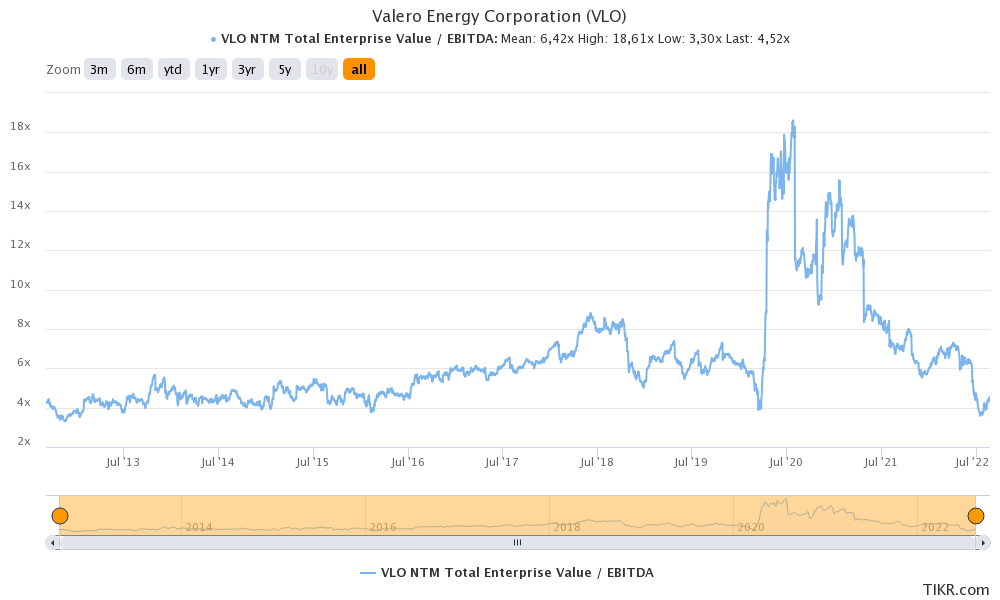

So, how expensive is VLO? According to my numbers, the company is trading at roughly 6.4x EBITDA. This is based on a $51.46 billion implied enterprise value consisting of its $46.7 billion market cap, $3.0 billion in expected net debt (pricing in 2023/2024 debt reduction efforts), and $1.76 billion in minority interest.

I used $8.0 billion in expected EBITDA as that’s what analysts believe the company can generate in a “normal” year after 2023. In other words, low expected net debt is the only thing I’m incorporating from current energy tailwinds.

This valuation is extremely fair and it includes a rather large margin of error. Especially because minority interest will come down as earnings normalize.

TIKR.com

With that said, there’s a major headwind: demand.

As most know, inflation is sky-high. The Fed is determined to fight inflation but unable to directly impact supply, which is the core issue of inflation. It cannot print available labor, it cannot drill for oil, and it cannot lower transportation costs – to name three examples.

The Fed can, however, harm demand, which is one way to deal with inflation. Hence, the Fed is hiking aggressively into economic weakness, which is hurting economic growth indicators even more.

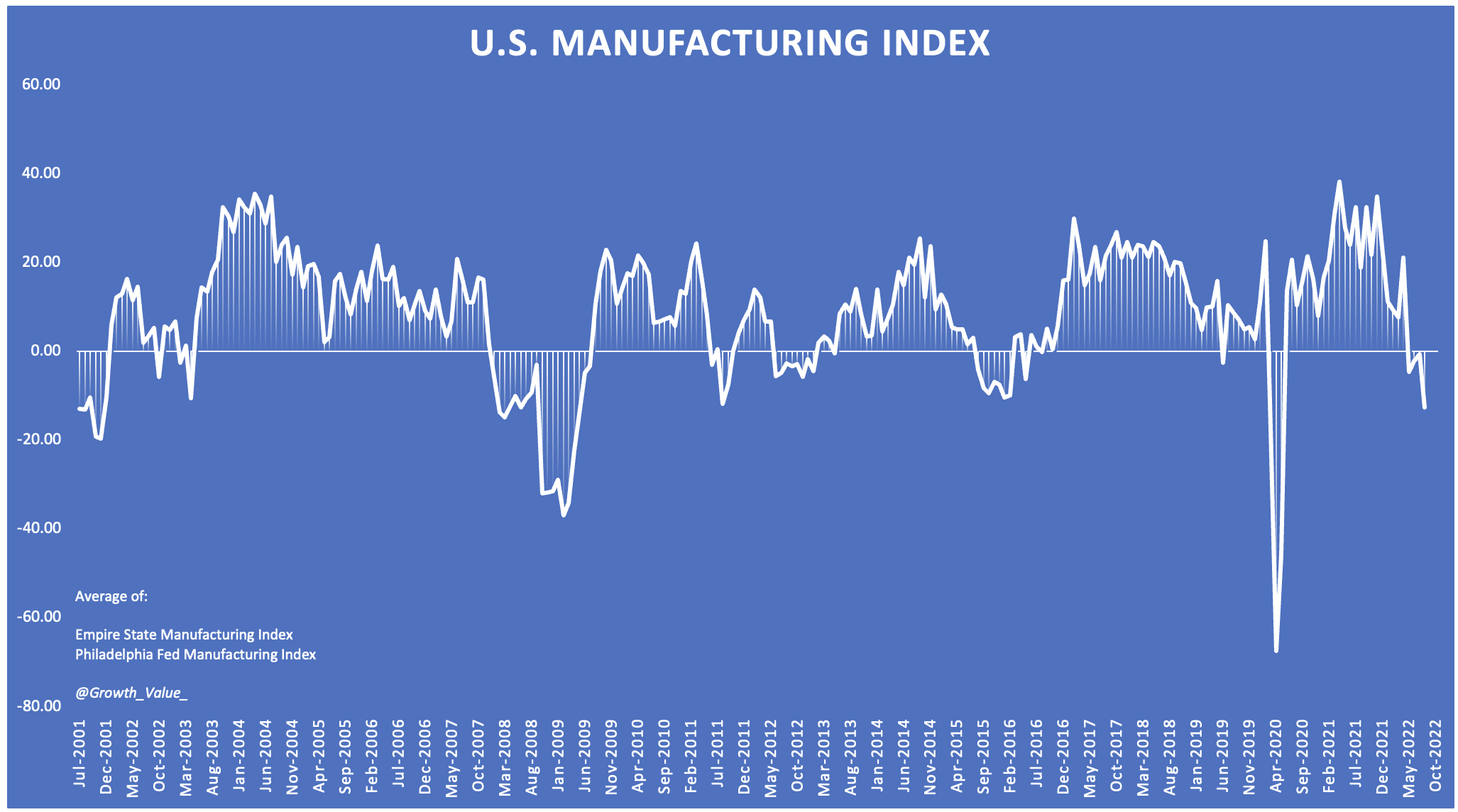

My manufacturing indicator shows a steep decline in economic activity, which could be made worse as the Fed is expected to hike rates to at least 3.50% going into next year.

Author (Empire State/Philadelphia Fed)

While refinery margins look good for the foreseeable future, which could cause investors to de-risk their portfolios, meaning selling some stocks like Valero, which still depend on throughput volumes.

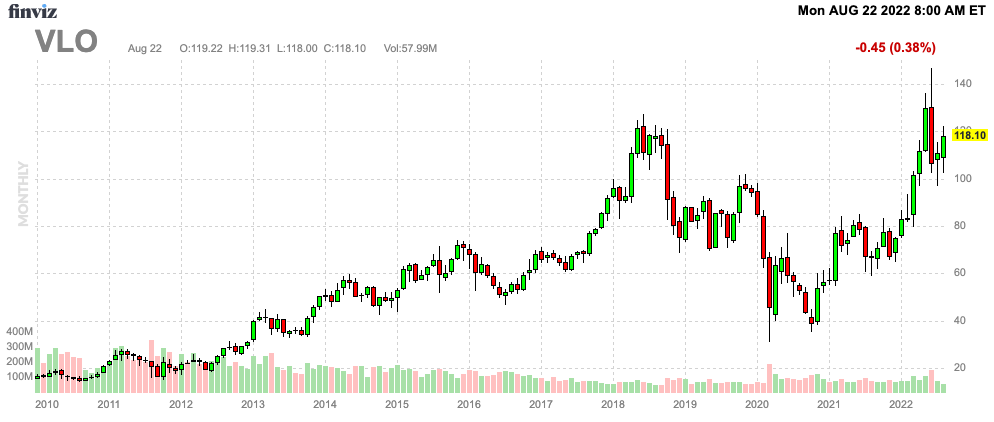

In other words, while I remain bullish, I wouldn’t bet against a short-term pullback to $100 if selling picks up again.

FINVIZ

This brings me to the takeaway.

Takeaway

Valero is truly one of my favorite dividend stocks on the market. The company has a high yield and the ability for long-term (aggressive) dividend growth. This makes it a fantastic stock for growth-oriented investors who like to add some higher yield to their portfolios.

Especially now, Valero remains in a fantastic spot to accelerate debt repayment, which will put management in a position to finally start hiking its dividend again. Buybacks have started to improve again as free cash flow is much higher than anyone could have anticipated going into this year.

The valuation is low and it allows for more upside. However, economic demand risks are rising, which could offset some of the benefits from higher (supply-related) margins.

The bottom line is that I’m consistently adding to VLO. Its high yield and shareholder-friendly approach make it a fantastic long-term investment. It’s just important for (potential) investors to always be aware of VLO’s above-average volatility. Unlike conservative, low-volatility, dividend stocks, VLO has the ability to “annoy” investors with regular steep drawdowns.

Yet, thanks to its ability to bounce back, long-term total returns are what make VLO a truly special dividend stock.