Will Tesla’s Stock Split Trigger Another 80% Run-Up?

Table of Contents

On March 28, Tesla ( TSLA 3.39% ) made headlines when management announced at an annual shareholder meeting that it intends to seek shareholder approval for a stock split. While the split details weren’t disclosed, when the stock last split in 2020, it split 5-for-1. With Tesla stock trading around $1,000 per share, a similar split would mean each share would be valued at around $200.

This mechanism works by cutting how much each share is was worth by a fifth and instantaneously paying a dividend of four additional shares, so stock owners are made whole. Tesla’s last split triggered an epic 80% run-up in the stock price between the announcement and the actual split in August 2020.

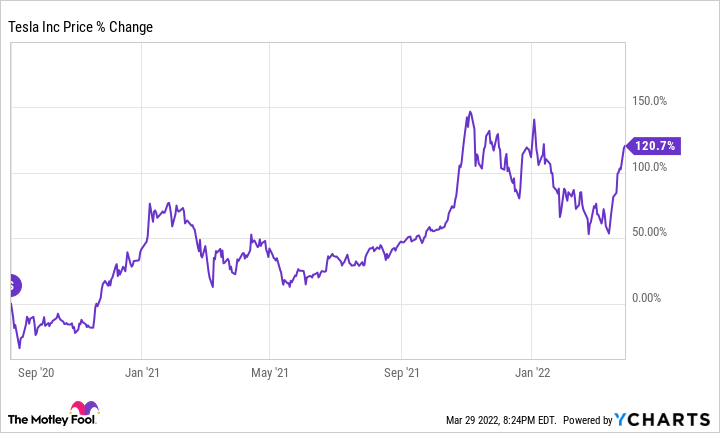

TSLA data by YCharts. Stock split was announced on Aug. 11, 2020 and occurred on Aug. 31, 2020.

Anyone who purchased the stock prior to the announcement and held on through the split made an incredible 80% return in less than a month. However, since Aug. 31, 2020, the stock is up an additional 120%, including the price correction that occurred right after the last split finalized.

TSLA data by YCharts

The split may have been a positive catalyst in the short term, but the business performance is what has propelled shares further over the past year and a half. With the positive direction of Tesla’s business, investors should be excited about its execution and plans rather than any upcoming split.

The leader in electric vehicles

Tesla has been doubted by many people during its existence. Regardless of what your opinion is of CEO and founder Elon Musk or the company’s business practices, Tesla has brought electric vehicles (EVs) into the mainstream. In the fourth quarter of 2021, Tesla delivered 308,600 EVs. Not too shabby when compared to General Motors‘ ( GM 0.49% ) 26 EVs delivered in Q4 or Ford Motor Company‘s ( F -0.60% ) 27,410 Mustang Mach-E’s delivered during all of 2021.

Image source: Tesla.

Tesla is the clear leader in the U.S. EV race at the moment. With the long-awaited Cybertruck likely launching in 2022, Tesla will have another catalyst to boost sales, although it will be late to the electrified truck party behind Rivian and Ford.

While Tesla is dominating domestically, it has much stiffer competition on the global stage.

| Manufacturer | 2021 Total EV Production | Market Share |

|---|---|---|

| Tesla | 936,712 | 14.4% |

| Volkswagen (Germany) |

757,994 | 11.7% |

| SAIC Motor (China) |

683,086 | 10.5% |

| BYD (China) |

593,878 | 9.1% |

Source: InsideEVs.

While still the leader, Tesla has some capable competitors overseas, which makes sense as EVs are not a winner-take-all industry. At its current capacity, Tesla can produce just over 1 million vehicles annually in its factories in California and Shanghai. However, it has factories in Berlin and Texas coming online that will increase its capacity as market demand widens. While not giving specifics, management expects 50% annual growth in vehicle deliveries over a “multi-year horizon.”

With increased production, investors should be excited about Tesla’s future expansion plans.

Improving financials

Tesla has come a long way since nearly declaring bankruptcy on Christmas Eve 2008. The company has more than $17.6 billion in cash with only $5.2 billion in debt on its balance sheet as of Dec. 31. Overall in 2021, Tesla produced $5 billion in free cash flow, showing its ability to survive without external funding.

Many bears said Tesla could never be profitable and that it was propping up its business by selling its energy credits, but they have been proven wrong. Tesla generated only $314 million from credits during Q4, down 22% year over year. It also generated a 14.7% operating margin according to generally accepted accounting principles (GAAP), a value that is nearly triple Ford’s 5.4% and GM’s 4.5% operating margins. This increase in operating efficiency allowed Tesla’s earnings per share (EPS) to rise 754% to $2.05 in Q4. Tesla’s business is both profitable and growing quarterly revenue quickly at a 71% year-over-year clip; both factors are delivering those bearish on the stock a crushing defeat.

The valuation

One point for Tesla bears is the stock’s extreme valuation. Tesla stock trades at a sky-high price-to-earnings (P/E) ratio of 219 and at 347 times free cash flow. Considering legacy automakers Ford and GM trade at P/Es of 3.7 and 6.4, respectively, Tesla’s valuation seems rather inflated.

However, Tesla is no legacy automaker. Its direct-to-consumer business model gives it margin advantages, and Tesla has other ambitions in the solar roof and battery pack space. With Musk steering the company, it’s unclear what venture Tesla will expand into next. While some may consider this a bad characteristic, others embrace the idea.

Image source: Tesla.

Regardless, the valuation of the business is the primary investment risk right now. Buying even a great business at the wrong price can lead to suboptimal investment returns.

With Tesla’s profit margin steadily rising throughout 2021 as well as growing its revenue, the stock’s valuation will come down as time passes on.

With an excellent business in a growing market, Tesla makes a great investment. Because of the high valuation, it may be smart to ease into the stock over time. Tesla stock is volatile and has suffered several corrections along the way to its current high valuation. And if the stock reacts as it did during the 2020 stock split, waiting may not be the best decision for investors. While I don’t believe the stock will have the same 80% run-up it did in 2020, I’m confident it can continue excelling.

This article represents the opinion of the writer, who may disagree with the “official” recommendation position of a Motley Fool premium advisory service. We’re motley! Questioning an investing thesis – even one of our own – helps us all think critically about investing and make decisions that help us become smarter, happier, and richer.